Apple has lowered its component orders by as much as 10 percent, according to our teams in Asia. The cuts seem to be driven by weak demand for the new iPhone 6s.

In response, Apple’s stock fell by over three percent.

Who knows – the report may well turn out to foreshadow a drop in iPhone sales. However, consider that Apple’s CFO, Luca Maestri, forecasted that Apple will likely grow iPhone sales this quarter on their earnings call last week.

The way I can best explain these kinds of reports – without any firsthand knowledge but with strong suspicion – is that these investment companies do this to talk a stock down in order to give their clients an opportunity to buy the stock at a better price. Call me cynical, but it happens all… the… time.

“That [is] all good and well until you learn it’s not Bakken but Kurdish oil, under strict embargo. Well done [for] supporting ISIS,” the consultant replied by e-mail.

You can absolutely be run over if you don’t continue to pioneer. If you ever see yourself as doing maintenance, then you will be run over.

Taking that quote out of context and reading it as a general, cautionary idea makes it powerful. It’s especially applicable to those in the tech world, but also more widely.

First, let me say that linking to a typical sensationalist Forbes article is probably not going to happen on this blog very often, but there are echoes here of others who question how successful the Apple Watch has been, and so I think this merits some thought.

The gist of this article is that since Apple is offering a program in some San Francisco and Boston area stores to buy an Apple Watch with an iPhone and get a $50 overall discount, things are going badly. Moreover, since Apple is not breaking out sales figures for the watch, this is a sign that they are hiding this bad news somehow:

Tim Cook won’t offer exact sales figures because the only insights competitors will glean is that if Apple has failed to ignite consumer demand with a halo product, then they surely can’t with a rival offering.

Apple has always said, even before they sold a single unit, that they would not be breaking out sales figures for Apple Watch. Let’s admit, though, that the watch is not going to light the world on fire as the iPhone has. It is never going to be that kind of blockbuster product, at least in its current incarnation. But there is not much analysis or real numbers in this Forbes piece:

Interest in wearables in general is declining. A report by Kantar Worldpanel ComTech in August this year reversed the notion that Apple Watch and wearable tech are extremely popular with the finding that only 3 percent of the U.S. population age 16 and older owns a smartwatch or smart fitness band. This is also in line with previous Gartner IT predictions that the market would slow in 2015 owing to conflicts between different types of fitness bands and because smartwatches offer the same functions.

Well, let’s do that same “analysis” for the PC industry, which declined in the past quarter – as it has in the past several quarters – while Apple’s Mac sales increased this past quarter by almost ten percent, and in each of the past several quarters by varying rates. If Apple didn’t break out Mac sales separately, I wonder if the same people in a tizzy about watch sales would be saying similar things based on looking at the overall PC industry trend. Or, on a slightly different plane but still squarely in the realm of speculation, let’s predict Apple’s chances in the mobile phone industry in 2007 based on the existing landscape of other products. That would have surely predicted an iPhone flop. And in fact, that was predicted by many.

Sometimes we don’t have enough data to do a good analysis. And for the Apple Watch, that’s the situation. Trying to fill in the blanks only with speculation can be interesting, but that doesn’t make it valid.

Where the iPhone’s ports are perfectly aligned, the A9’s look like they were machined by a drunk 6-year-old with a jackhammer. The headphone jack curls around the back edge. The charging port is off-center horizontally and vertically. And none of the holes is quite the same size or shape.

HTC presumably doesn’t want you to notice that the front-facing camera doesn’t align with the speaker, or that the proximity sensor appears to have been thrown on there randomly. HTC certainly doesn’t want you wondering why it felt the need to put a big logo on the front of the phone when there’s already a huge one on the back.

As with the design, the A9’s software feels like a good idea only half-finished…

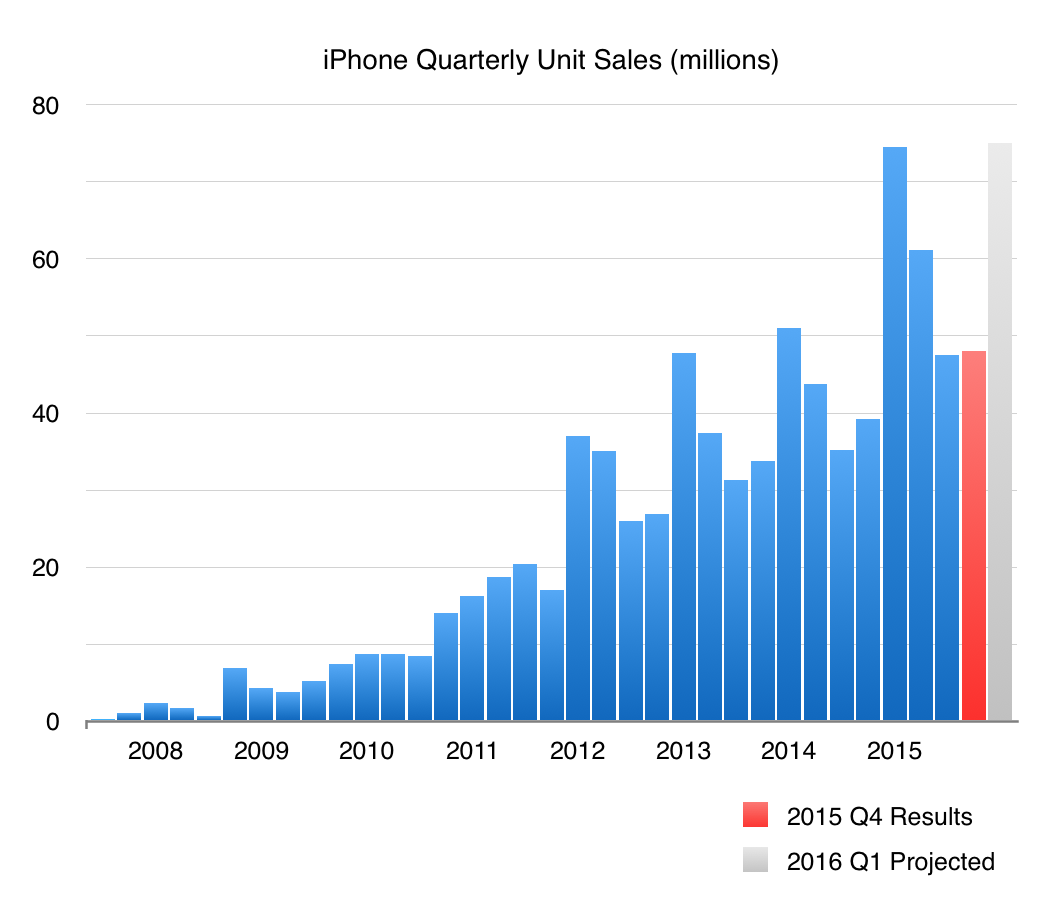

2016 Q1 Revenue Guidance: between $75.5B and $77.5B

So why am I focusing on iPhone unit sales here and in the previous post? There are a couple of reasons.

First, Tim Cook stated on today’s call that a key objective is adding more customers. The driver of Apple’s growth in recent years is due to one product – iPhone. As the iPhone goes, so goes Apple, at least in the short and medium term. How many phones they sell is a good way to track that. Note that average selling price has been trending up slightly.

Second, iPhone sales as a percentage of total revenue have increased steadily over the past three years:

2013: 53.1%

2014: 56.0%

2015: 65.9%

By the way, the highest percentage of iPhone sales to revenue was the first two quarters of the 2015 fiscal year, 68.6% and 69.4%, respectively.

To forecast a wide range of unit sales for 2016 Q1, we could take the lowest percentage of iPhone quarterly sales in 2015 to total revenue (62.5% in Q4, the most recent quarter) and the low end of next quarter’s guidance ($75.5B), and then take the highest percentage of iPhone quarterly sales in 2015 to revenue (69.4% in Q2) and the upper end of guidance ($77.5B) – and use the Q4 average selling price reported today ($670/unit) – and come up with very rough range:

2016 Q1 iPhone unit sales forecast: Between 70.4 million and 80.3 million

Yes, that’s a wide range. The consensus is that iPhone unit sales crack the 74.5 million mark from last year’s holiday quarter, which is right in the middle of this 70 to 80 million range. I think the thing to watch for, though, is iPhone unit sales topping the 79 million mark next quarter. That’s pretty small year-over-year iPhone unit sales growth, about a 6% increase. “We think we can grow iPhone (sales) during the December quarter,” Chief Financial Officer Luca Maestri told The Associated Press. So… let’s put that out there.

If the consensus ~75 million iPhone unit sales figure does end up being correct, and if Apple does come in at the high end of its total revenue guidance, it will probably be due to an increase in Apple Watch sales.

As always, buzz about the quarterly financial results for Apple is all over the map. Apple will report fiscal 2015 Q4 results at 5pm EST today. They are up against a so-called “tough comp” from 2014 Q4, which is when they started selling the iPhone 6 and 6 Plus in China. This quarter’s results will include two days of Chinese sales of the new iPhone 6s and 6s Plus.

Though the stock still remains cheaper than most other technology stocks that exploded higher on Friday, Apple can still get hurt. Cramer has noticed that Apple’s stock has been creeping up in anticipation of the quarter, so he will be on alert for any bruising, since the tech bar is set so high.

It really comes down to is what the guidance is for December. If they guide at the high end of the range…that’s going to be a sign that Apple’s optimistic that the [iPhone] ‘S’ cycle is going to be better than what investors think.

Where Apple’s stock price will end up after they report earnings is anyone’s guess – it almost always goes lower immediately after.

Longer term: Apple’s current price/earnings (P/E) multiple of 13 or so makes it a “cheap” stock compared to others in the tech-ish field:

</img>

</img>

</img>

</img>